Contents

- 1 What are B2B payments and why do they matter?

- 2 What is the difference between B2B and B2C payments?

- 3 How do B2B payments drive global economic growth?

- 4 What are the common B2B payment methods in B2B commerce?

- 5 What are the major challenges in B2B payments and how to overcome them?

- 6 Trends shaping the future of B2B payments

- 6.1 1. The digital payment revolution accelerates

- 6.2 2. Security becomes a competitive differentiator

- 6.3 3. Automation eliminates human error and delays

- 6.4 4. Real-time payments become the new standard

- 6.5 5. Mobile and IoT integration expand payment possibilities

- 6.6 6. AI and machine learning optimize payment strategy

- 7 How tariffs can possibly influence B2B payments

- 8 Choosing and implementing the right B2B payment solutions

- 9 Streamline your B2B payments with Wizcommerce

- 10 Frequently Asked Questions (FAQs) on B2B Payments

B2B payments are the backbone of wholesale and distribution businesses, yet they’re often plagued by inefficiencies, manual processes, and rising costs. In fact, 45% of businesses cite manual review as the biggest problem they face in B2B payments, while nearly 1 out of 3 B2B transactions are still done by cash and checks, highlighting just how outdated many payment systems remain.

The urgency for change is clear: 92% of financial institutions servicing B2Bs are actively digitizing their payment solutions to address these bottlenecks. Meanwhile, the global B2B payments market is projected to reach $241.8 trillion by 2031, driven by innovations in digital infrastructure, automation, and customer expectations.

Whether you’re a manufacturer, distributor, or wholesaler, understanding how B2B transactions work and how they’re evolving is critical to maintaining healthy cash flow and building scalable operations.

In this guide, we’ll break down the most effective B2B payment methods, help you overcome common challenges in B2B ecommerce wholesale payments, and reveal the latest trends that successful wholesale businesses are using to stay competitive.

What are B2B payments and why do they matter?

B2B payments refer to financial transactions made between businesses for goods or services. While consumer payments are typically instant and simple, B2B payments involve larger transaction amounts, extended payment cycles, and complex terms including invoicing process, credit arrangements, and purchase orders.

Why efficient B2B payments are essential for business success

Enhanced cash flow management: Modern B2B payments systems provide clear visibility into outstanding receivables and upcoming obligations, enabling better financial planning and working capital optimization.

Significant cost reduction: Manual B2B payments processing costs businesses approximately $25 per invoice, while automated digital systems reduce this to under $5 per transaction while eliminating errors that cause disputes and delays.

Competitive advantage: Organizations with streamlined B2B payments processes can offer more favorable payment terms to customers and negotiate better conditions with suppliers, creating measurable advantages in competitive markets.

Improved business relationships: Efficient B2B payments reduce transaction friction, increase transparency, and demonstrate operational reliability—all critical factors in building and maintaining strong business partnerships.

Enhanced security and compliance: Modern B2B payments platforms incorporate advanced fraud protection, regulatory compliance features, and comprehensive audit trails that safeguard business operations.

The evolution of B2B payments from basic transaction processing to strategic business capability directly impacts operational efficiency, profitability, and long-term growth potential.

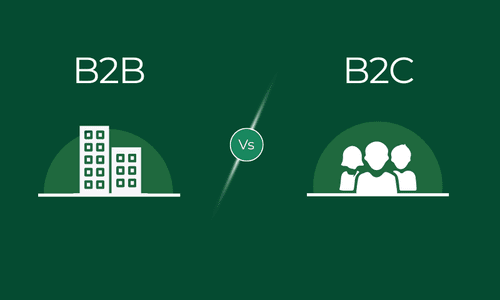

What is the difference between B2B and B2C payments?

Understanding the fundamental differences between B2B payments and B2C payments is crucial for choosing the right payment strategy for your business. While consumer payments prioritize speed and convenience, B2B payments must accommodate complex business relationships, extended credit terms, and sophisticated approval processes.

Here’s how B2B payments compare to consumer transactions:

| Aspect | B2B payments | B2C payments |

| Transaction volume | Typically lower in volume but higher in transaction value | Higher volume of transactions with lower value |

| Payment terms | Extended payment terms (30, 60, 90 days) | Immediate or short-term payments |

| Decision making | Involves multiple stakeholders and approval processes | Individual and impulsive buying decisions |

| Regulatory compliance | Stricter regulations, more complex invoicing requirements | Less stringent, simpler invoicing |

| Relationship focus | Long-term, relationship-driven negotiations | Often one-time, transactional interactions |

| Customization | Highly customized payment agreements and terms | Standardized payment methods and terms |

Now that we understand how B2B payments differ fundamentally from consumer payments, let’s explore their critical role in the global economy.

How do B2B payments drive global economic growth?

B2B payments are at the heart of global commerce, facilitating the exchange of goods and services between businesses across the world. According to Statista’s Worldwide Digital Payments research, the global digital payments market has reached $10.64 trillion in 2024. In this vast landscape, B2B payments are integral to operational efficiency and economic growth. Here’s how:

- Facilitate international trade: B2B payments make it possible for businesses to trade across borders, allowing them to engage with suppliers and customers worldwide, thereby boosting global commerce.

- Support supply chain management: Timely and efficient payment systems ensure smooth operations within supply chains, helping businesses manage orders, payments, and inventory seamlessly.

- Enhance financial planning: With reliable B2B payment processes, businesses gain better visibility into their financial position, enabling more accurate forecasts and helping in long-term strategic decision-making.

- Promote economic stability: Efficient B2B payments contribute to broader economic stability by ensuring that businesses can reliably settle transactions, fostering healthy business ecosystems.

- Drive innovation and technology adoption: The global scale of B2B payments encourages companies to adopt cutting-edge technologies, such as blockchain and AI, to process transactions more securely, quickly, and efficiently.

- Enable better liquidity management: By streamlining payment flows and improving the timing of transactions, B2B

payments help companies manage their liquidity more effectively, ensuring they have the necessary funds to operate without delays.

These factors highlight how b2b ecommerce wholesale payments are not just about settling invoices. They are the essential drivers of business efficiency, technological progress, and global economic growth.

What are the common B2B payment methods in B2B commerce?

When B2B payments need to happen, the methods and procedures vary widely, providing different benefits based on the business’s needs. Here’s a detailed look at the types of B2B payment methods you might consider:

1. Checks

Best for: Businesses requiring detailed paper trails and traditional accounting processes

While checks might seem outdated, they remain relevant in certain B2B payments scenarios. Many businesses still prefer checks for their clear documentation and the control they provide over payment timing. Checks work well when you need physical records for compliance or when dealing with vendors who haven’t modernized their payment acceptance.

Consider checks when: You’re working with traditional suppliers, need detailed audit trails, or require payment timing control.

2. ACH Payments (Automated Clearing House)

Best for: Recurring payments and cost-effective bulk transactions

ACH payments have become a cornerstone of efficient B2B payments because they offer significant cost advantages over other digital payment methods. They’re particularly valuable for recurring supplier payments, payroll processing, and any situation where you need reliable, automated fund transfers. ACH also works well for larger transaction amounts where credit card fees would be prohibitive.

Consider ACH when: You need recurring payment automation, want to reduce transaction costs, or are processing larger payment amounts.

3. Wire Transfers

Best for: High-value, time-sensitive, and international transactions

Wire transfers remain the gold standard for B2B payments when speed and security are paramount. They’re especially valuable for international business relationships and large, one-time transactions where immediate settlement is crucial. While more expensive than other methods, wire transfers provide certainty and immediate finality.

Consider wire transfers when: You’re making international payments, need immediate settlement, or are handling high-value transactions where speed matters more than cost.

4. Credit Cards

Best for: Smaller transactions and businesses needing immediate cash flow

Credit cards offer unique advantages in B2B payments, particularly for smaller purchases and situations where immediate payment is beneficial. They provide built-in fraud protection, detailed transaction records, and can help with cash flow management. However, transaction fees make them less practical for larger amounts.

Consider credit cards when: You’re making smaller purchases, need immediate payment confirmation, or want built-in purchase protection.

5. Digital Payment Platforms and Digital Wallets

Best for: Modern businesses prioritizing speed and integration

Digital platforms have revolutionized B2B payments by combining the convenience of consumer payment apps with business-specific features. These platforms often integrate seamlessly with accounting software and provide real-time transaction tracking. They’re particularly effective for businesses operating in digital-first environments.

Consider digital platforms when: You need seamless software integration, want real-time payment tracking, or are working with tech-forward business partners.

6. Electronic Funds Transfers (EFT)

Best for: Streamlined digital operations and automated workflows

EFT encompasses various digital B2B payments methods including ACH and wire transfers, representing the broader shift toward electronic payment processing. EFTs are essential for businesses looking to automate their payment workflows and reduce manual processing overhead.

Consider EFT when: You want to digitize payment operations, need automated processing capabilities, or are scaling your payment volumes.

The most effective approach often involves using multiple B2B payments methods strategically. Consider your transaction patterns, relationship requirements, and operational priorities when building your payment strategy. Many successful businesses combine ACH for recurring payments, wire transfers for urgent or international transactions, and digital platforms for everyday vendor payments.

The key is matching each B2B payments method to its ideal use case rather than trying to force one solution for every situation.

Having the right payment methods available is essential, but even the best options can’t overcome fundamental process problems that plague many B2B operations.

What are the major challenges in B2B payments and how to overcome them?

Several challenges can arise in B2B payments, but by addressing them through technological advancements and strategic practices, businesses can improve the efficiency of their B2B payment processes, reduce costs, and maintain healthier supplier relationships. Let’s look at these challenges first:

| Challenge | Problem | Solution |

| High Processing Fees | Manual handling and data entry create administrative burdens and increased costs, especially for high-volume businesses | Implement automated B2B payment systems to streamline operations and reduce manual processing |

| Fraud Risk | Electronic transactions face threats from payment interception, invoice fraud, and sophisticated scams | Deploy advanced security measures: two-factor authentication, encryption, transaction monitoring, regular audits, and employee training |

| Payment Delays | Lengthy approval processes and inefficient systems strain supplier relationships and disrupt cash flow | Adopt streamlined processes: electronic invoicing, automated payment systems, and clear communication of payment terms |

| Limited Visibility | Traditional methods lack transparency, making transaction tracking difficult and dispute resolution challenging | Integrate modern B2B payment platforms with real-time tracking, reporting features, and unified transaction views |

1. Excessive Processing Costs

Manual B2B payments processing is bleeding money from your business. Every paper check requires handling, storage, data entry, and reconciliation—creating a cascade of administrative costs that add up quickly. Manual data entry errors compound the problem, requiring corrections that delay payments and frustrate suppliers.

For high-volume businesses, these inefficiencies become exponentially more expensive. The solution is clear: automated B2B payments systems eliminate most manual touchpoints, dramatically reducing processing costs while improving accuracy and speed.

| Implement digital payment automation that handles data entry, processing, and reconciliation automatically, freeing your team for higher-value work. |

2. Growing Risk of Fraud Threats

As B2B payments become online payments, fraudsters are following the money. Today’s threats go far beyond simple payment interception—sophisticated criminals are creating fake invoices, impersonating suppliers, and exploiting weak security protocols to steal millions from unsuspecting businesses.

The financial impact extends beyond direct losses. Fraud incidents damage supplier relationships, create compliance headaches, and can result in legal liability. Modern B2B payments platforms combat these threats with a multi-layered level of security including encryption, real-time monitoring, and behavioral analysis.

| Deploy comprehensive security features including two-factor authentication, encrypted transactions, continuous monitoring, and regular employee training on fraud recognition. |

3. Payment Delays That Damage Relationships

Late payments are relationship killers in B2B commerce. When your B2B payments consistently arrive after agreed terms, suppliers notice. They may start demanding upfront payment, reduce credit limits, or simply take their business elsewhere. The ripple effects can disrupt your entire supply chain.

The root cause is usually inefficient approval workflows and outdated payment systems that create bottlenecks. Suppliers understand that businesses have processes, but they also have their own cash flow requirements and operational needs.

| Streamline approval processes with electronic invoicing, automated payment scheduling, and clear communication channels. Set realistic payment terms and stick to them consistently. |

4. Lack of Financial Visibility

Traditional B2B payments methods operate in the dark. You might know money went out, but tracking the specifics—payment status, approval stages, outstanding invoices—becomes a manual detective process. This opacity leads to duplicate payments, missed discounts, and frustrated finance teams.

Without real-time visibility, resolving payment disputes becomes time-consuming and relationship-damaging. Modern B2B payments platforms solve this with comprehensive dashboards that show exactly where every payment stands in your workflow.

| Implement payment platforms with real-time tracking, automated reporting, and unified dashboards that give all stakeholders instant access to payment status and history. |

These B2B payments challenges aren’t just operational inconveniences—they directly impact profitability, supplier relationships, and business growth.

The good news is that modern payment technology addresses all four issues simultaneously, delivering cost savings, enhanced security, improved relationships, and complete visibility in one integrated solution.

Trends shaping the future of B2B payments

As B2B payments evolve, numerous trends are transforming the way businesses handle financial transactions. Let’s dive into the key trends driving the future of B2B payments:

1. The digital payment revolution accelerates

Why it matters: Traditional payment methods are becoming liability

The shift toward digital B2B payments isn’t just a trend—it’s an inevitable business evolution. Wire transfers, e-wallets, and virtual credit cards are replacing checks and cash because they deliver measurable advantages: faster processing, lower costs, and better tracking. Businesses still relying heavily on paper-based B2B payments are already at a competitive disadvantage.

2. Security becomes a competitive differentiator

Why it matters: Payment security directly affects business partnerships

As B2B payments move online, security excellence separates market leaders from laggards. Advanced encryption, multi-factor authentication, and blockchain integration are becoming standard expectations rather than premium features. Businesses with superior B2B payments security win more partnerships and command better terms.

3. Automation eliminates human error and delays

Why it matters: Manual processes can’t scale with business growth

Automated B2B payments systems are transforming finance departments from cost centers into strategic assets. By automating invoicing, processing, and reconciliation, businesses dramatically reduce errors while accelerating payment cycles. The data insights from automated systems enable more strategic financial decision-making.

4. Real-time payments become the new standard

Why it matters: Payment speed affects supplier relationships and negotiations

Instant settlement capability is becoming a baseline expectation in B2B payments. Real-time processing gives businesses more flexibility in cash flow management and strengthens supplier relationships. Companies offering real-time B2B payments often negotiate better terms and secure preferred supplier status.

5. Mobile and IoT integration expand payment possibilities

Why it matters: Payment flexibility drives operational efficiency

Mobile-enabled B2B payments and IoT integration are removing location and device constraints from financial transactions. Field sales teams, warehouse operations, and remote workers can all process payments seamlessly. This flexibility is particularly valuable for businesses with distributed operations or frequent travel requirements.

6. AI and machine learning optimize payment strategy

Why it matters: Predictive capabilities provide competitive intelligence

Artificial intelligence is transforming B2B payments from reactive processing to predictive optimization. AI systems analyze payment patterns, predict cash flow needs, and identify fraud risks before they impact operations. Machine learning continuously improves payment timing and method selection based on historical performance.

Understanding technology trends is only half the equation for successful B2B payments planning. External economic and policy factors can dramatically influence payment timing, methods, and costs. For businesses engaged in international trade, tariffs represent one of the most significant external forces affecting payment strategy.

How tariffs can possibly influence B2B payments

Global trade policies, particularly tariffs, can significantly impact B2B payments planning for businesses engaged in international commerce. Understanding these effects helps companies adapt their payment strategies proactively.

Key impacts on B2B payments:

Cost adjustments: Tariffs increase import costs, often requiring businesses to renegotiate payment terms. Suppliers may request higher upfront payments or different payment schedules to manage increased expenses.

Payment method shifts: Trade uncertainties may push businesses toward more secure payment options like letters of credit or escrow accounts, which provide protection against policy changes but can slow payment processing.

Currency considerations: Tariff-related market volatility affects exchange rates, making it more challenging to predict final payment amounts for international transactions.

Supply chain adaptation: Businesses may need to switch suppliers to avoid tariff costs, requiring new B2B payments relationships and terms with alternative partners.

Documentation complexity: Enhanced customs requirements can delay payments when goods are held up in clearance or when tariff rates change during transit.

The key for businesses is staying informed about trade policy changes and maintaining flexible B2B payments processes that can adapt to shifting international trade conditions.

Choosing and implementing the right B2B payment solutions

Selecting the right B2B payment solution requires careful evaluation and strategic implementation. Here’s your practical guide to making the right choice and ensuring successful deployment.

Security & Compliance

- PCI-DSS certification and SOC 2 compliance

- Multi-layer encryption for all transactions

- Real-time fraud monitoring and alerts

- Regular security audits and updates

- Comprehensive audit trails for compliance reporting

Integration Capabilities

- Native integration with your existing ERP system

- Real-time data synchronization

- API access for custom integrations

- Seamless accounting software connectivity

- Mobile compatibility for field teams

Customer Experience

- Intuitive interface requiring minimal training

- Fast transaction processing times

- Offline functionality for trade shows

- Customizable workflows and approval processes

- Multi-device accessibility

Business Features

- Multiple payment method support (ACH, cards, bank transfers, wire transfers)

- Automated invoicing and reconciliation

- Flexible payment terms management

- Comprehensive reporting and analytics

- Scalability to handle business growth

Once you’ve identified a platform that meets these evaluation criteria, the next critical step is ensuring smooth implementation. Even the best payment solution can fail without proper planning and execution.

Here are some best practices to ensure seamless implementation.

Start small and scale gradually – Begin with a pilot group of customers rather than full deployment to identify and resolve issues early.

Prioritize training and support – Invest time in comprehensive team training and ensure ongoing support is readily available.

Maintain backup processes – Keep existing payment methods available during the transition period to avoid disruption.

Focus on integration quality – Ensure seamless data flow between your payment platform and existing business systems to avoid manual workarounds.

Plan for change management – Communicate benefits clearly to both internal teams and customers to encourage adoption.

While this evaluation framework helps identify the key criteria for any B2B payment solution, finding a platform that excels across all areas while offering industry-specific features can be challenging.

For wholesale distributors and manufacturers who want a solution that checks every box on this evaluation framework while delivering measurable results, the search often leads to specialized platforms built specifically for B2B commerce operations.

Streamline your B2B payments with Wizcommerce

WizPay by WizCommerce addresses every criterion on your evaluation checklist through a specialized platform designed for wholesale distributors and manufacturers. Built specifically for B2B operations, WizPay delivers the security, integration capabilities, and operational efficiency that modern wholesale businesses require.

Seamless Integration: Native sync with QuickBooks, Xero, and major ERP systems with automated account updates and real-time reporting

Complete Payment Flexibility: Support for ACH, credit/debit cards, payment links, and offline methods with custom payment terms

Enterprise Security: PCI-DSS compliant with end-to-end encryption, fraud monitoring, and comprehensive audit trails

Competitive B2B Processing Rates: Cost-effective transaction fees structured for wholesale transaction volumes

Multi-Device Accessibility: Full functionality across mobile, tablet, and desktop for field and office teams

Advanced Operations Management: Centralized dispute resolution and specialized features for complex wholesale transactions

Ready to modernize your B2B payment operations? Contact WizCommerce today to discuss your specific payment requirements and discover how WizPay can transform your business operations.

Frequently Asked Questions (FAQs) on B2B Payments

How are B2B payments made?

The process starts with a purchase order, followed by invoice generation after goods or services are delivered. The buyer reviews and approves the invoice internally, then processes payment through their preferred method. The seller receives payment, reconciles it with their financial records, and sends confirmation. Modern platforms automate most of these steps to reduce manual work and speed up longer payment cycles.

What security measures are in place for B2B payments?

B2B payment platforms use multiple security layers including encryption, tokenization, and multi-factor authentication. They maintain PCI-DSS compliance for credit card processing and employ real-time fraud monitoring. Role-based access controls limit system access, while comprehensive audit trails track all activities. Regular security audits and penetration testing help identify and address vulnerabilities.

What is the payment term B2B?

B2B payment terms define when and how business customers must pay for wholesale orders, typically ranging from immediate payment to Net 30, Net 60, or Net 90 days. These terms often include early payment discounts and credit limits based on the buyer’s relationship and creditworthiness.

What is B2B and B2C payment?

B2B payments occur between businesses (wholesaler to retailer) and typically involve larger order values, extended payment terms, credit management, and multiple approval workflows. B2C payments are direct consumer transactions with immediate payment processing, smaller amounts, and simple checkout flows.

How do I accept B2B payments?

Accept B2B payments through specialized platforms that support wholesale features like credit terms, ACH transfers, payment links, pre-saved company cards, advance payments, and integration with ERP systems. Ensure PCI compliance and offer multiple payment methods to accommodate different business preferences.

What is B2B payment example?

A furniture manufacturer selling to retail stores might offer Net 30 payment terms, accept a $50,000 order via purchase order, process payment through ACH transfer or company credit card, and provide credit-based refunds for returns—all managed through their B2B payment platform.